The non-obvious path to unusual success

By Brad Otto

“This just in: you can’t take the same actions as everyone else and expect to outperform.”

I was readingthis classic memo from Howard Marks today and I was struck by how timeless it is. Today in our industry the message is often summarized as “the only way to make money in venture is to be non-consensus and right.”

The basic logic is if you invest in the obvious and you are right, you invest with everyone else and you achieve average financial returns. Nobody ever got fired for buying Apple stock, and if your goal is to not get fired this is okay, at least in the short term. There are multi-billion dollar industries built on achieving average investment results (i.e. ETFs and venture capital megafunds). Strategic investors and corporate venture capital often fall into this category. They seek to invest in consensus-right and try not to make the company look bad. These organizations are typically measured on more than just financial returns, so average returns are sufficient.

However, Marks would say that if your goal is unusual success, it cannot be achieved through conventional means. Above market financial returns cannot be achieved by investing in the obvious. It’s important to note this is not as simple as being contrarian. One must be contrarian and one must be right.

The only way to achieve above-market returns is to invest in the non-obvious, the unusual, or the idiosyncratic.

The paradox of the healthcare industry is that it prefers the obvious, the usual, and the orthodox. There are serious consequences for painting outside the lines. Patient lives are at stake. Regulators are strict. This explains why the healthcare industry tends to adopt new technology slower than others.

Over time ideas naturally shift from one category to another. For example, take consumer genetics company 23andMe. When the company was founded in early 2006 it was definitely non-consensus, and I’d argue it was also wrong. The business model didn’t work at the time, considering the cost of sequencing a whole genome was over $10 million. However, over the next decade the cost of whole genome sequencing fell to $10,000 and then eventually to under $1,000. At those prices the company was non-consensus / right. The golden ticket. The investors whose timing was right achieved above market returns. Soon, the broader market caught up with the obvious trend and the company shifted to consensus / right. Today, you might argue that 23andMe has come full circle, falling back to non-consensus / wrong. The point is a company or investment idea does not remain in the same place over time. The framework is dynamic as markets adjust to new information.

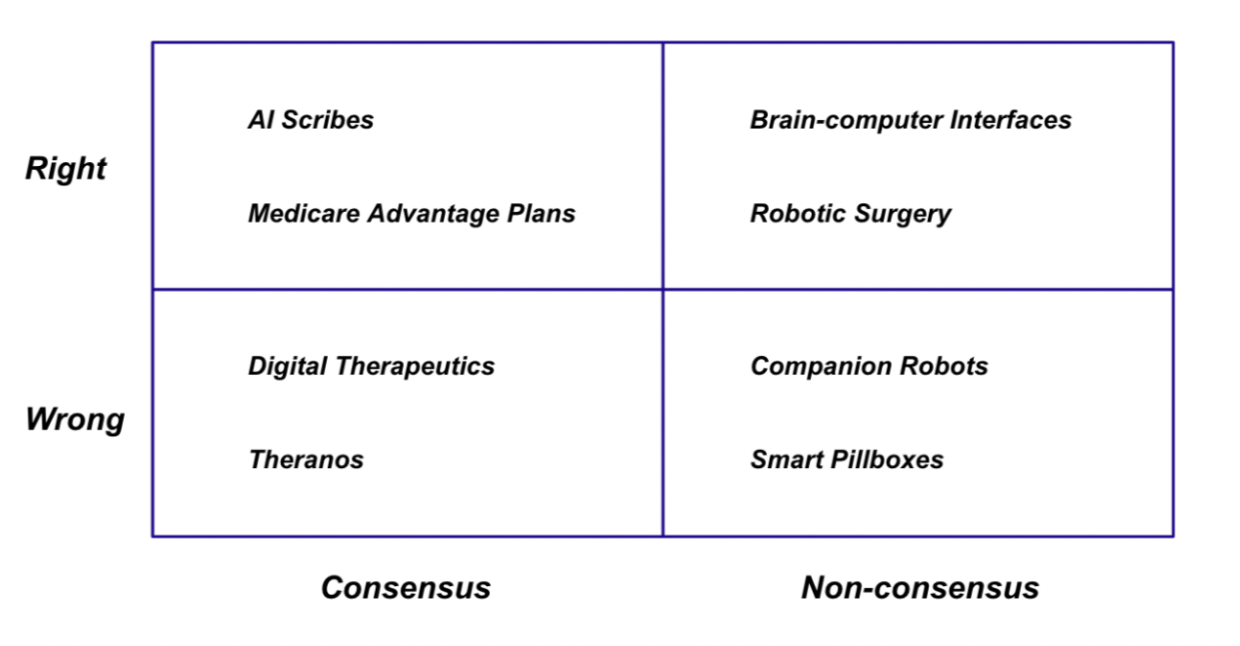

I couldn’t help but add my thoughts on today’s market by categorizing some popular healthcare themes in Marks’ framework. These are subjective and I’m sure many people will disagree. I’d love to hear your thoughts in the comments.

What companies/themes would you add, and where would you put them? What is non-consensus today that will be proven consensus / right over time?