Health Insurtech Investment Thesis

By Brad Otto

Health insurance is a crucial financial tool that helps individuals and families manage the costs associated with medical care. There are several types of health insurance coverage available in the U.S., including employer-sponsored insurance, government-sponsored plans, and individual or family plans purchased through the Health Insurance Marketplace.

The private health insurance industry in the U.S. is enormous, with $1.3 trillion dollars in premiums written in 2022.

Major players in the industry include national insurance companies like UnitedHealth Group, Cigna, and Aetna, as well as a long tail of regional insurers and smaller startup players. These companies compete for market share by offering plans with different levels of coverage, pricing, and benefits. Health insurance brokers and agents play a critical role in facilitating the purchase of insurance plans and providing guidance to individuals and businesses navigating the complex landscape of healthcare coverage.

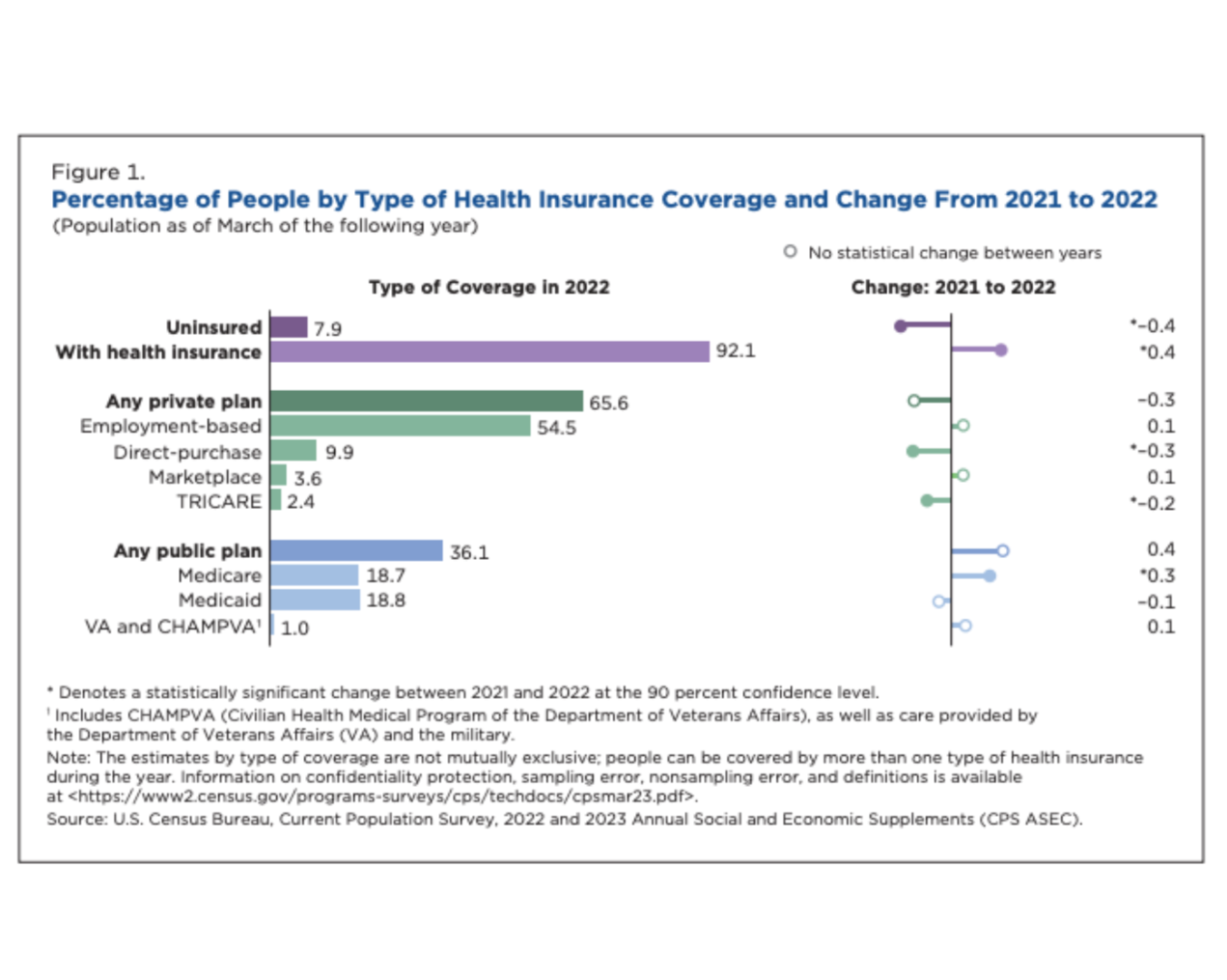

Private insurance remains the dominant form of coverage, providing health benefits to nearly 66% of Americans. Government-sponsored plans, such as Medicare for seniors and Medicaid for low-income individuals and families, play a crucial role in providing coverage to vulnerable populations. Over 36% of Americans are covered under government-sponsored plans.

Industry Challenges

Despite its size and diversity, the U.S. health insurance market faces ongoing challenges including rising healthcare costs, regulatory changes, and access disparities.

Rising Healthcare Costs

The cost of healthcare in the U.S. continues to increase, driving up premiums for individuals, families, and employers. In 2023, average premiums for single coverage reached $8,435, while family coverage averaged $23,968, both rising 7% in just one year.The average family premium has increased 22% since 2018 and 47% since 2013. This trend puts financial pressure on employers, employees, and individuals, making health insurance less affordable.

Regulatory Changes and Uncertainty

The health insurance industry is heavily regulated, and shifts in government policies—such as those related to the Affordable Care Act (ACA), Medicaid expansion, or Medicare reforms—create uncertainty. Insurers must continually adapt to new rules, which can affect coverage options, pricing, and business strategies.

Access Disparities and Coverage Gaps

Despite the various types of health insurance coverage available, significant disparities in access to healthcare persist. Low-income populations, particularly those in states with limited Medicaid expansion, and rural communities often struggle to access affordable insurance and healthcare services. This creates inequities in the system, leaving many individuals underinsured or uninsured. Nearly 8% of Americans are uninsured.

Future Opportunities

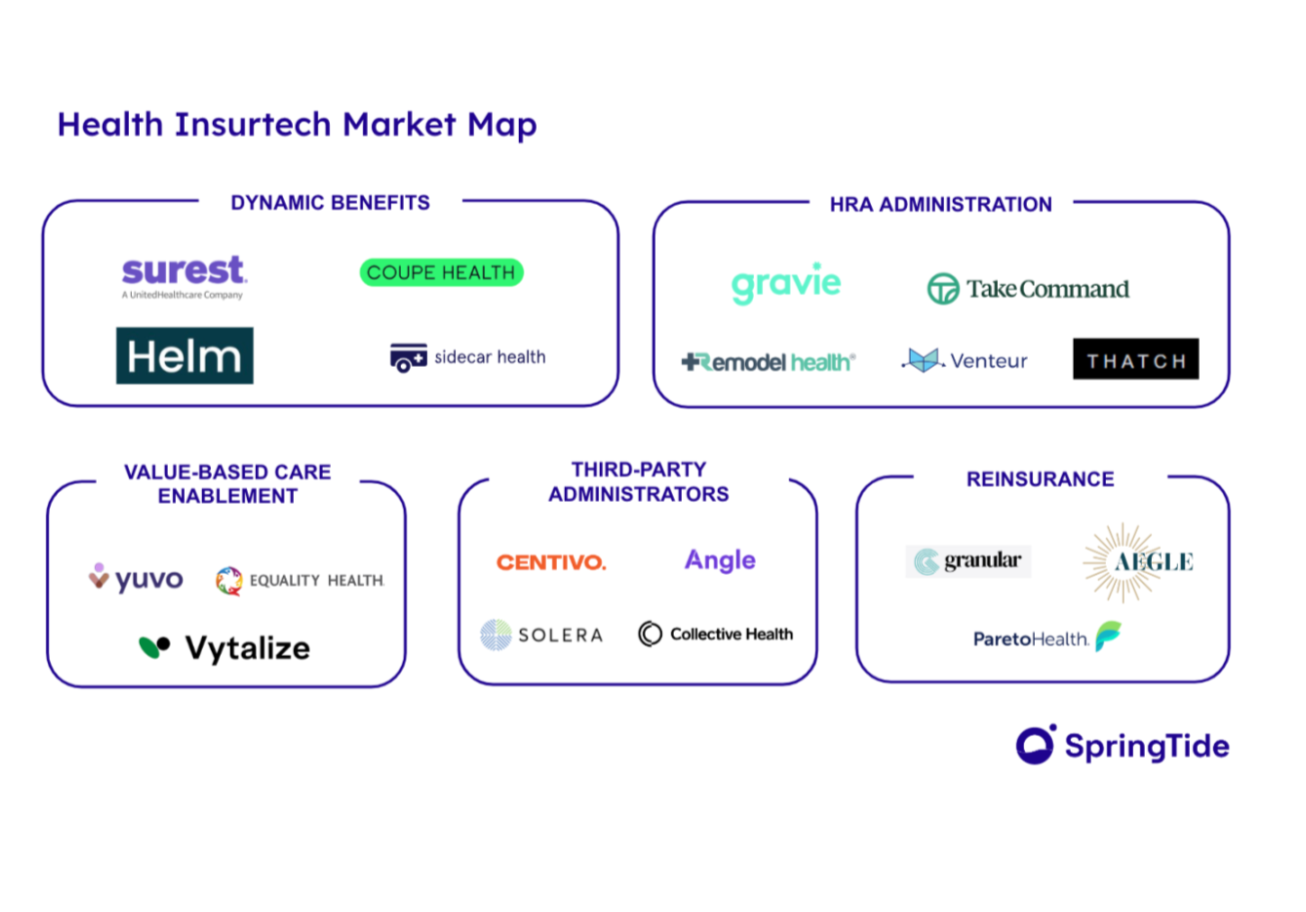

Amidst an evolving technological landscape and a trillion-dollar market, these challenges create highly attractive opportunities for entrepreneurs to disrupt established players. Here are the five areas of health insurance where we expect to see the most innovation in the coming decade.